The Intelligent Way to Convert 401K to Roth IRA for Early Retirees

Retirement investment accounts are complex. Some are pre-tax, some are post-tax. Some have penalties if you withdraw early, some allow you to withdraw up to a certain amount without penalty. Some require you to withdraw a minimum amount after the age of 70.5, some don't. And many others. In short, there's a lot of choices—and a lot of tradeoffs.

The average working professional will likely have multiple retirement accounts and will be tasked with figuring out how to manage them. Luckily the government has afforded us ways to convert one type of account into another. This means we can 1) consolidate accounts 2) simply convert them from one type to another or 3) consolidate and convert at the same time.

In this blog post, I will explain why and how I plan to convert my traditional 401K account into a Roth IRA, all while minimizing my tax burden. I will show that for high-income earners, who are planning to retire early, contributing to a Traditional 401k and eventually rolling it into a Roth IRA is the most effective strategy for building your retirement nest egg.

Before getting into the technicals of how I plan to do the conversion, let’s go over frequently asked questions on this topic.

What is a traditional 401K?

A traditional 401K is a retirement account that will allow you to save and invest untaxed income. That is, if you make $100K this year and you contribute $6K to your traditional 401K account, you will only be responsible for the taxes on the remaining $94K. When you withdraw from your traditional 401K account during retirement, you will then need to pay earned income taxes on the withdrawn amount for that year.

What is a Roth IRA?

A Roth IRA is a retirement account that will allow you to save and invest after-tax income. That is, if you make $100K this year and you contribute $6K to your Roth IRA account, you will still be responsible for the taxes on all $100K. But when you withdraw money from your Roth IRA account during retirement, you will not need to pay any taxes.

How is a traditional 401K different from a Roth IRA?

In a nutshell, a traditional 401K taxes you at the time of withdrawal (i.e. later) and a Roth IRA taxes you at the time of deposit (i.e. now). There are other differences such as (for most people) a 401K has a higher contribution limit of $19K/year but a Roth IRA has a contribution limit of only $6K. Additionally, there is no income limit for who can contribute to a 401K, but if you’re married and make over $203K, you will not be able to directly contribute to a Roth IRA. Generally, IRAs have more flexible investing options.

Why would one want to convert to a Roth IRA?

The two biggest reasons to convert a Roth IRA is to 1) avoid the required minimum distribution (aka RMD) requirement and 2) increase the number of investment options. It depends on the 401K, but generally, it is limited to Target Funds and Mutual Funds. Most of them will have high fees.

Is it possible to convert a Traditional 401K into a Roth IRA?

Yes, absolutely. This kind of conversion is common. What most people don’t realize is that you can actually convert just a portion of your Traditional 401K into a Roth IRA.

Which one is better?

For most Americans, directly contributing to their Roth IRA is the best option. However, if you’re a high-income earner or plan to retire early, contributing to a traditional 401K followed by a Roth IRA conversion is the superior option. I will use the remaining portion of this blog to illustrate why.

Consider the following two strategies:

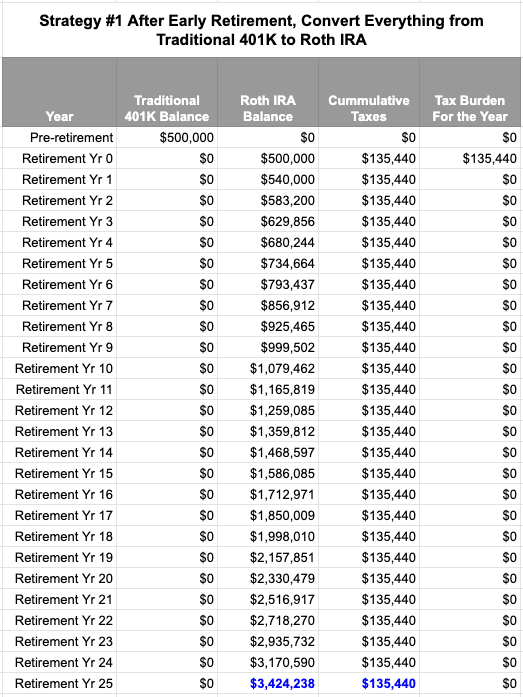

Strategy #1: $500,000 contributed to Traditional 401K, then converted to Roth IRA all at once

Strategy #2: $500,000 contributed to Traditional 401K, then gradually converted to Roth IRA over a 26-year span

Figure 1.1

If you were to employ strategy #1, the Roth IRA account will end up with over $3.4M at the end of 26 years. And you’ll end up paying $135K in taxes at the time of conversion. Not too shabby. Strategy #1 is what most people end up doing because it’s simple. However, check out what strategy #2 looks like:

Figure 1.2

If you were to employ strategy #2, the Roth IRA account will end up with over $3.4M at the end of 26 years—same as strategy #1. But the total taxes paid is only $119K, compared to $135K. More importantly, the tax burden is spread across a 26-year time span. To illustrate the significance of this, have a look at the right-most column in Figure 1.2. There are 2 key insights that brings this together:

The US tax system is progressive. So the more money you make in a year, the higher your effective tax rate will be. In this case, converting from a Traditional 401K to Roth IRA is considered a “taxable event." Instead of making $500K in one year and nothing over the next 25 years, it’s better to spread it out. The effective tax rate will be lower, as a result.

Instead of paying $135K upfront in taxes, you only pay $4,660 per year—enough to cover the conversion of $40K. But to have a true apples-to-apples comparison, you will need to analyze what would happen if you were to reinvest the difference ($130,780). That is, in Year 0 instead of paying $135K in taxes (strategy #1), you will pay $4.6K in taxes and invest the other $130.8K (strategy #2). And in subsequent years, you will withdraw an additional $4.6K from that investment to cover the taxes. Assuming an annual rate of return of 8%, the investment will end up being $600,757 pre-tax over the course of 26 years. Therefore, the true difference between strategy #1 and strategy #2 is $600,757 in opportunity cost!!! This is a significant amount considering the initial account was worth $500K and the final account value is $3.4M.

Once your money is in a Roth IRA, you won’t ever need to worry about taxes or worry about being required to withdraw from it when you’re 70.5 years old. Also, at the time of your death, your inheritor(s) will be able to take that amount of money as a lump sum, tax free!

In conclusion, assuming you have multiple years to do this kind of conversion, strategy #2 is the best way to maximize your retirement savings. Since I plan to retire at 35 years old and don’t plan to touch this money until 70 years old, I will have 35 years to convert. This means my tax burden will be even smaller!

If you enjoy this content, please consider following me on my Facebook Page for the latest and subscribing below!